Research

Student Financial Savvy Eroding

- By Dian Schaffhauser

- 04/03/15

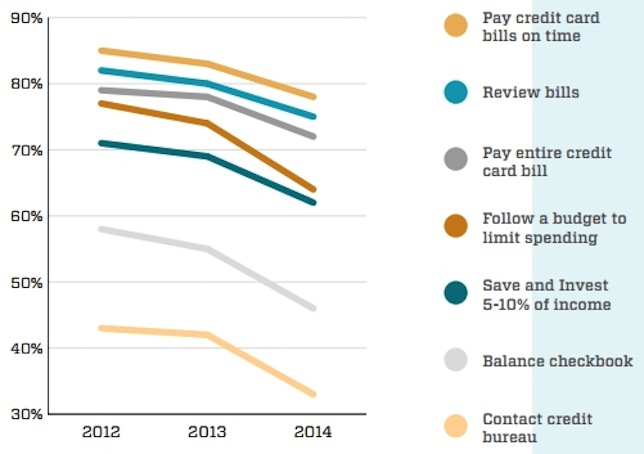

College students aren't as bright as they think they are regarding finances. Although they're more likely to have a credit card and a

checking account than they were in 2012, they're also less likely to pay their credit bills on time or in full or to follow a budget. On top

of that, they're more likely to have more than a single credit card and to carry larger balances and less likely to review their bills or

credit history, let alone to save or invest even five percent of what they earn.

Among four-year students, only 62 percent check their account balances; 12 percent don't because they're "too nervous." Additionally, 16

percent of student respondents live paycheck to paycheck and yet only 72 percent stop spending when their bank account balances were low.

This year's "

Money Matters on Campus" survey questioned 43,000 college students across institutions in the United States about their money practices for

the third year in a row, and the results were eye-popping. The financial attitudes of college students "displayed more materialism, more

compulsion, less caution and less aversion to debt as time spent on campus increased," the report stated.

The survey asked students to answer six questions related to their financial literacy, such as, "As a general rule, how many months'

expenses do financial planners recommend that you set aside in an emergency?" Those who had a checking account tended to show better results

than those who didn't. Among two-year students, who did the best, those with bank accounts answered 2.54 questions correctly vs. 1.97 for those

without bank accounts. That suggests, the report's authors said, that "increased experience with 'transactional' accounts for high school

students would be of great benefit to promoting self-efficacy."

The issue of debt is a big one for this segment. Compared to three years ago, students reported that they were more likely to take out

student loans, but less likely to plan for paying off their loans, making their payments on time or consolidating their loans.

The report was compiled by Higher One and

EverFi, two companies that have a business interest in the topic of student finances.

Higher One provides payment, refund disbursement and other services to colleges and universities, as well student debit cards. EverFi provides

financial education programs for students and adults.

Currently, the researchers said, "more than half of those with student loans report being concerned about their ability to repay the debt."

As the report pointed out, along with steady increases in tuition rates, new graduates "face an unstable job market." Those between 21 and 24

have an 8.5 percent unemployment rate and a 16.8 percent underemployment rate.

Community college students are more likely to worry about financial issues than four-year students, the research found. While community

college students reported fewer (44 percent vs. 63 percent) and smaller student loan balances than their four-year counterparts, they were

also more likely to have multiple credit cards with higher outstanding balances. Also, while exactly half of four-year students said they were

concerned about having enough money to last the semester, 58 percent of two-year students said the same. And while 46 percent of four-year

students were worried about being able to afford their next year at school, that count was 58 percent for two-year students.

In spite of the fact that a growing number of states require high schoolers to either take a financial literacy class (17 states) or pass a

financial literacy test (six states) before they can graduate, the students themselves report feeling less prepared to manage their money than

any other challenge they face in college life. While 73 percent said they could keep up with coursework, only 58 percent said they were

prepared to manage money. (Those who took those high school courses on personal finance were 10 percent more likely to say they could manage

their money.)

"Students reported feeling least prepared for the financial aspects of college, even as student loan debts continue to grow at an alarming

rate," said Mary Johnson, vice president of financial literacy and student aid policy at Higher One, in a statement. "The results suggest we

must start financial literacy education before students enter college and continue to teach its importance throughout a student's college

career — it is imperative that students know the impact student loan debt can have later in life."

About the Author

Dian Schaffhauser is a former senior contributing editor for 1105 Media's education publications THE Journal, Campus Technology and Spaces4Learning.